When conflict erupts in the Middle East, the world's packaging industry pays attention, not because it is a direct combatant, but because the region sits at the crossroads of energy, raw materials, and the sea lanes that carry global trade. The current escalation has accelerated disruptions that were already testing supply chains, and packaging manufacturers from Bangalore to Birmingham are revising their cost models.

01

Quick Facts at a Glance

02

Raw Material Exposure by Packaging Type

Each packaging format carries a different risk profile — split between direct petrochemical dependency and indirect exposure through freight and fuel costs.

03

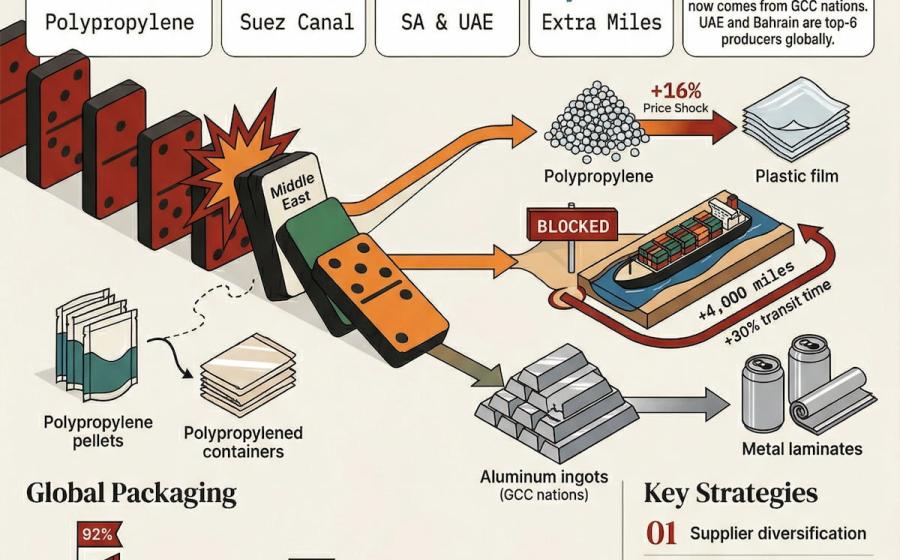

Middle East & Gulf Share of Global Inputs

through Suez Canal

(Saudi Arabia + UAE)

(Saudi Arabia + UAE)

(Middle East region)

(GCC nations)

04

Shipping Disruption — Before & After

Standard route

Diverted route

Energy

Logistics

Materials

Metals

Oil price — the first domino

The most immediate pressure point is energy. Packaging is an energy-intensive business, from the furnaces that melt aluminum to the extruders that form plastic film. With Brent crude jumping sharply in the opening days of renewed conflict and analysts flagging the risk of further climbs, the cost of manufacturing packaging materials is rising at every stage of the process. Higher fuel costs also feed directly into freight rates, compounding the pain for companies that ship finished packaging or move goods in packaged form.

"The label printing industry relies heavily on global supply chains for materials derived from petrochemicals — volatility in these markets affects the price and availability of key substrates."

— Director of Operations, Mercian Labels

Petrochemicals under pressure

Plastic packaging, the dominant format globally, is built from petrochemical feedstocks, particularly polypropylene and polyethylene. Saudi Arabia and the UAE together account for roughly a fifth of global polyethylene trade, and close to the same share of polypropylene. Since the latest escalation, prices for both polymers have moved sharply upward. For packaging companies, these are not discretionary inputs: polypropylene films wrap snack foods and pharmaceuticals; polyethylene is the backbone of flexible pouches, shrink wrap, and bags. There is no quick substitute.

Aluminum: a quieter vulnerability

Metal packaging, cans for beverages, foil laminates for food, faces a different but equally real challenge. The Middle East has become a significant global aluminum producer over the past decade, with Gulf Cooperation Council nations now supplying roughly 8% of world production. The UAE and Bahrain rank among the top six producing countries globally. For North American and European can-makers, this matters: the region supplies about a fifth of U.S. aluminum imports. With supply under strain, aluminum prices have moved noticeably higher since hostilities deepened.

Shipping routes add cost and time

Beyond raw materials, logistics is a growing burden. The Red Sea crisis of 2024 showed just how quickly a regional flare-up can re-route global commerce. Ships forced to sail around the Cape of Good Hope instead of through the Suez Canal added roughly 4,000 miles and around 30% more transit time to every journey. Those lessons are fresh in carriers' minds. Airspace disruptions in the region have further tightened cargo capacity, with airlines re-routing to avoid conflict zones, reducing available space and pushing up air freight rates for time-sensitive packaging deliveries.

05

How the Industry Is Responding

The packaging sector is not standing still. Companies are diversifying their supplier networks, building strategic buffer stocks of key substrates, and investing in greater visibility across multi-tier supply chains. For fiber-based packaging, corrugated boxes, cartons, the direct material exposure is lower, but rising fuel prices still filter through as higher freight costs. Across the board, manufacturers are recognizing that the era of lean, just-in-time procurement from concentrated regional sources carries meaningful risk.

The longer-term question is whether this period of volatility accelerates the shift toward locally sourced materials, bio-based plastics, and recycled content, inputs that are less tethered to Middle Eastern energy markets. For now, most companies are focused on managing the immediate cost environment. But the strategic case for supply chain resilience has rarely been stronger.

The speed and scope of escalation has highlighted just how unstable the region can become in as little as 48 hours, and how exposed global manufacturing remains.